Intelligent Investment

Multifamily Buyer Sentiment Improves in Q3

Q3 2025 Multifamily Underwriting Survey

October 22, 2025 3 Minute Read

Buyer sentiment for core and value-add multifamily assets improved in Q3, while underwriting assumptions mostly held steady, according to CBRE’s Q3 Multifamily Underwriting Survey. The shift in positive sentiment comes as the Federal Reserve cut interest rates for the first time this year in September. Investment volume is expected to improve in coming quarters. In addition, there may be incremental compression in cap rates as long-term bond rates stabilize and the Fed further cuts interest rates.

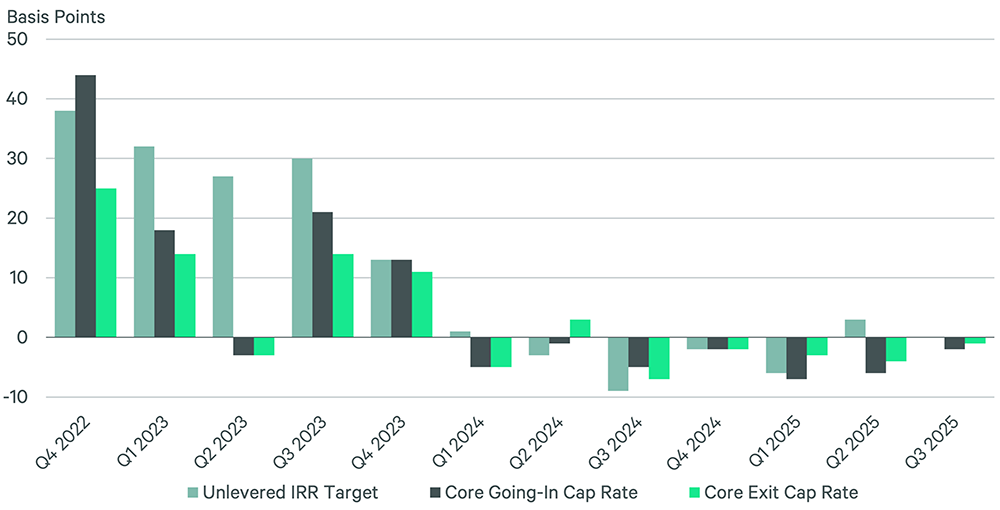

Figure 1: Quarterly Changes in IRR Target & Cap Rates for Core Assets

The average core multifamily going-in cap rate fell by 2 basis points (bps) to 4.73% in Q3, while the average exit cap rate fell by 1 bp to 4.95%. Core unlevered internal rate of return (IRR) targets remained at 7.70%.

Core underwriting metrics are now in line with those in early 2023. The spread between going-in and exit cap rates for core assets increased to 22 bps in Q3. The spread is expected to increase over the next two years, with going-in cap rates compressing more than exit cap rates as the Fed cuts interest rates. However, it may be some time before the spread increases to a more typical level of between 50 and 60 bps.

Fifteen of the 19 markets tracked by CBRE had stable IRR targets for core assets in Q3. Two markets (Chicago and Nashville) saw a decrease in their core-asset IRR targets, while Austin and Dallas saw an increase.

Figure 2: Buyer & Seller Sentiment for Core & Value-Add Assets

Source: CBRE Research, Q3 2025.

Core-asset buyer sentiment improved in Q3, with 64% of survey respondents expressing a positive outlook vs. 57% in Q2. Negative sentiment was unchanged at 5%. Core buyers were substantially more positive than they were at the end of 2024. Value-add buyer sentiment improved the most, jumping to 70% positive from 62% in Q2. Value-add sellers remained largely neutral, with both minimal positive and negative sentiment. Overall buyer and seller sentiment improved most in Sun Belt markets such as Atlanta, Miami and Nashville.

Figure 3: Buyer Valuation Underwriting Assumptions for Core & Value-Add Multifamily Assets

Underwriting assumptions of annual asking rent growth over the next three years for core assets held steady at 2.8%, while those for value-add assets decreased slightly to 3.2%. This aligns with the deceleration in rent growth in many markets in Q3.

For value-add assets, going-in cap rates increased by 3 bps to 5.23% and exit cap rates remained at 5.38%. The spread between the two fell slightly to 15 from 18 bps. Unlevered IRR targets for value-add assets compressed for the seventh consecutive quarter to 9.49%.

Figure 4: Underwriting Assumptions for Core & Value-Add Multifamily Assets by Market, Q3 2025

Note: Estimates are based on the expert opinion of local CBRE investment professionals.

Source: CBRE Research, Q3 2025.

Four markets saw going-in cap rate compression for core assets (Atlanta, Miami, Nashville and Seattle), while Denver and Tampa saw slight increases. No markets saw more than a 25-bp movement either way. For value-add assets, Chicago and Nashville had lower going-in cap rates in Q3 than in Q2, while Dallas had a 31-bp increase.

While core and value-add buyer sentiment improved in Q3, overall underwriting metrics held relatively firm. Many investors remained reluctant to sell, even with high demand for multifamily assets causing more aggressive bids and the bid-ask spread narrowing. However, we expect more multifamily investors to sell in Q4 and next year as buyers take advantage of a more liquid debt market with attractive financing options.

Related Insights

-

Approximately 1.8 million U.S. renter households can no longer afford the median-priced home in their market due to less affordability of homeownership over the past five and a half years.

-

Brief | Intelligent Investment

Pre-Stabilized Properties Limit Overall Multifamily Rent Growth

June 25, 2025

Despite multifamily vacancy rates largely stabilizing nationwide in 2024, year-over-year rent growth still lags pre-pandemic levels.