Report | Intelligent Investment

2026 Asia Pacific Investor Intentions Survey

February 3, 2026 10 Minute Read

Executive Summary

Looking for a PDF of this content?

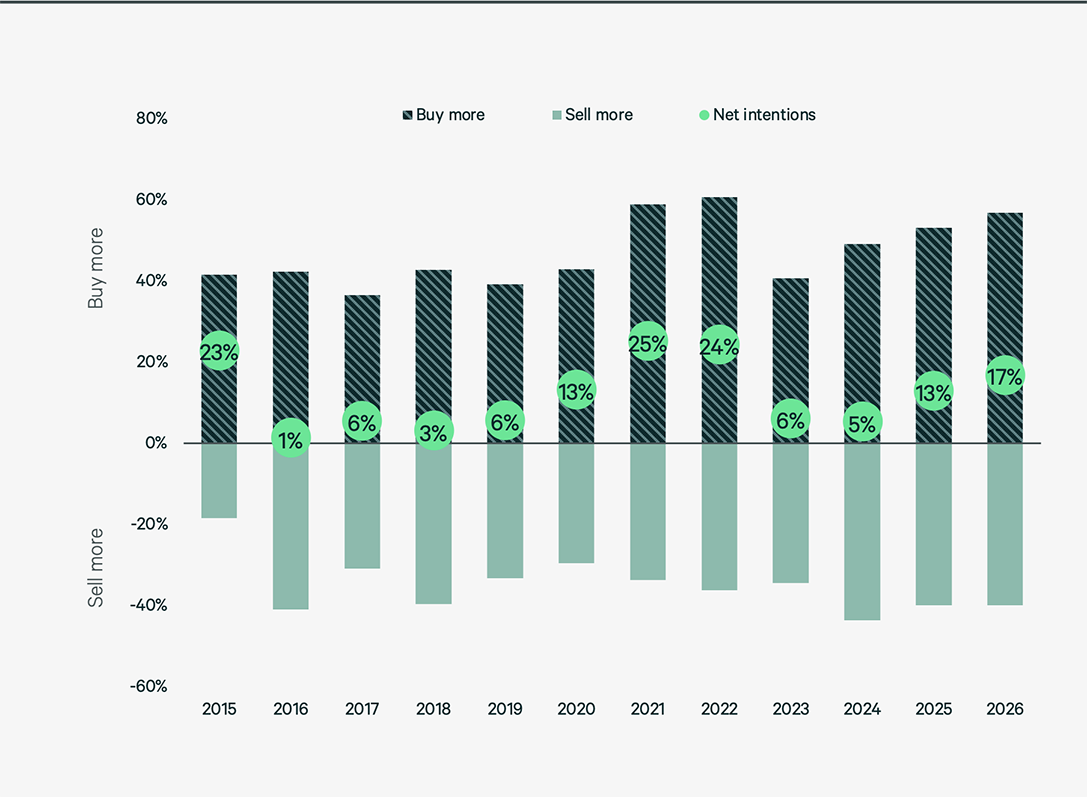

CBRE’s 2026 Asia Pacific Investor Intentions Survey uncovered a further improvement in buying intentions across most markets in Asia Pacific this year, with over 57% of respondents indicating their preference to buy more real estate in 2026.

Net buying intentions in Korea, Australia and Singapore strengthened while those in Japan remained stable. While their intentions remained negative, investors in both mainland China and Hong Kong SAR exhibited improved net buying intentions in 2026 compared to last year.

Sector preference shifted in this year’s survey. Offices rose to become the most preferred sector for the first time in six years, with industrial & logistics and the living sector rounding out the top three. Data centres continue to climb up the list of investor preferences, placing fourth this year.

This year’s survey was conducted in November and December 2025. Over 420 responses were received from participants who were asked a range of questions related to their buying intentions, perceived challenges and preferred strategies, sectors, and markets for the coming year. This report summarises their responses and explains what this means for the Asia Pacific commercial real estate market in 2026.

Other key findings:

- Sentiment: Overall investment sentiment continues to improve, with net buying intentions increasing from 5% in 2024, to 13% in 2025 and 17% in 2026. Investors indicated that strong occupier demand, a reduced supply pipeline and lowering of debt costs are the main tailwinds for investment in 2026.

- Strategy: The survey revealed that core-plus and value-added investment strategies gained further traction among investors in 2026. Investors believe they can achieve core-plus and possibly value-add returns from core product as their rental growth conviction grows stronger. Interest in opportunistic strategies continues to weaken.

- Asset Class: Offices overtook industrial and logistics as the top sector in 2026 for the first time in six years, with markets providing strong rental growth such as Australia, Japan and Singapore identified as the most sought after locations. The living sector remains popular, with build-to-rent opportunities attracting strong interest. Data centres climbed to fourth place.

- Alternatives: Healthcare assets remain top of mind for investors considering alternative assets. Emphasis on living sector assets, such as retirement living and student accommodation, continues to grow. Interest in infrastructure rose modestly this year.

- Destinations: Tokyo retained top spot as the preferred market for cross-border investment for a seventh consecutive year, followed by Sydney, then Singapore and Seoul (tied). Hong Kong SAR returned to the top five following a brief hiatus.

- Sustainability: Investors ranked retrofitting existing buildings of green buildings above acquisition and development as their top sustainability option in 2026. Although progress remains gradual, investors continue to place a higher green premium on ESG-certified assets.

Investor Buying and Selling Intentions

Net buying intentions improve across the board

Net buying intentions reached 17% in this year's survey, driven by improvements in Korea, Australia and Singapore, and stable buying intentions in Japan. While still negative, both mainland China and Hong Kong SAR investors showed improved net buying intentions in 2026 compared to 2025.

Regional investors in Singapore and Hong Kong SAR, alongside landlords with significant AUM in Australia and Korea, displayed the biggest change in net buying intentions this year. This cohort identified the stronger rental outlook and improving occupier activity as the primary reason behind their stronger willingness to buy.

This year CBRE expects investors to place a particularly strong focus on core-plus assets, which are set to experience strong rental growth as cap rate compression slows. Japanese investors will remain net buyers in 2026, showing stronger net buying intentions this year, with domestic investment activity expected to remain robust.

Investment sentiment among domestic mainland Chinese investors, while still negative, improved in 2026. An increasingly diverse domestic investor base, which includes state-backed insurance companies, shored up transaction activity in 2025, offsetting a decline in foreign investment.

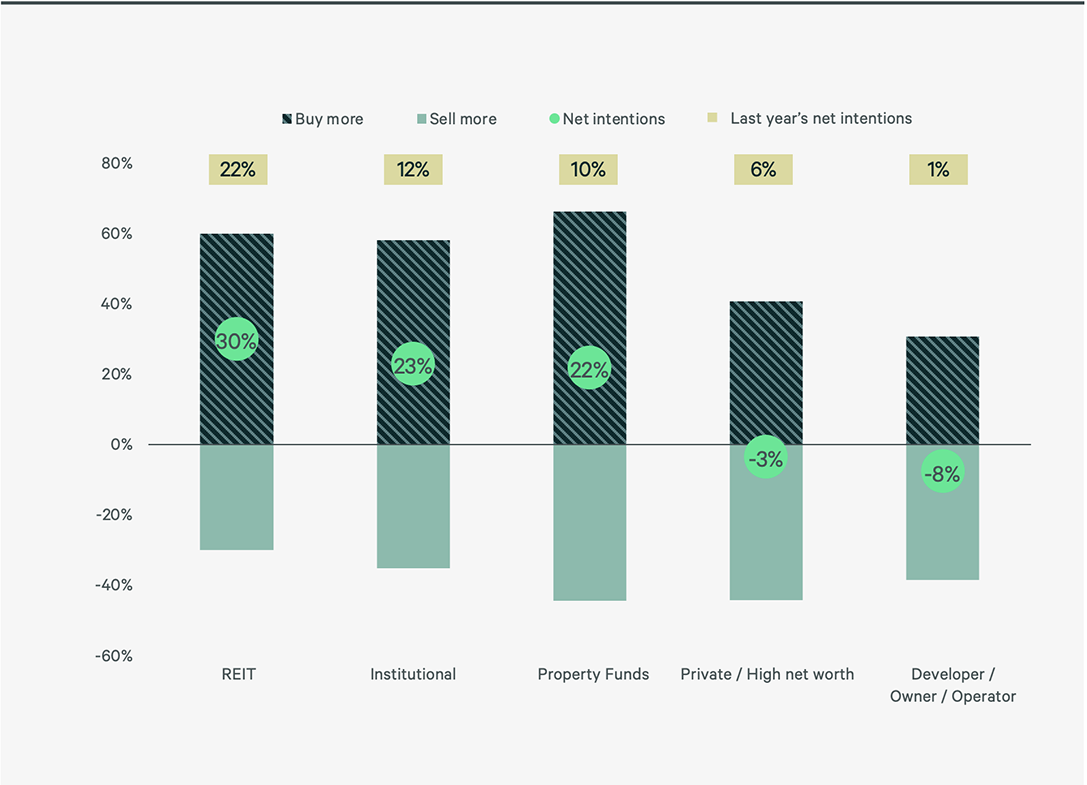

REITs, institutional investors and funds more active buyers in 2026; privates/developers to be net sellers

Asia Pacific REITs had delivered total returns of over 22% for the full year 2025, according to the Global Property Research and Asia Pacific Real Assets Association (APREA) REIT Composite Index. This is providing a strong foundation for REITs to be net buyers in 2026, with net buying intentions from this cohort reaching +30% in this year’s survey.

Investment by private equity funds, real estate funds and institutional investors including insurance companies, pension funds and sovereign wealth funds picked up in 2025, with expectations that positive momentum will continue in 2026.

On the flipside, private investors could turn from net buyers to net sellers in 2026 as they look to recycle assets acquired during the period of price dislocation that occurred 24 months ago. Net intentions for this cohort stood at -3% in 2026, down from +6% in 2025.

Significant increases in construction costs and enduring debt costs for development in markets such as Australia and Korea resulted in a decline in developers’ net buying intentions in 2026. One bright spot is corporate owner-occupiers in Greater China turning more active in buying office assets for self-use, particularly in Hong Kong SAR.

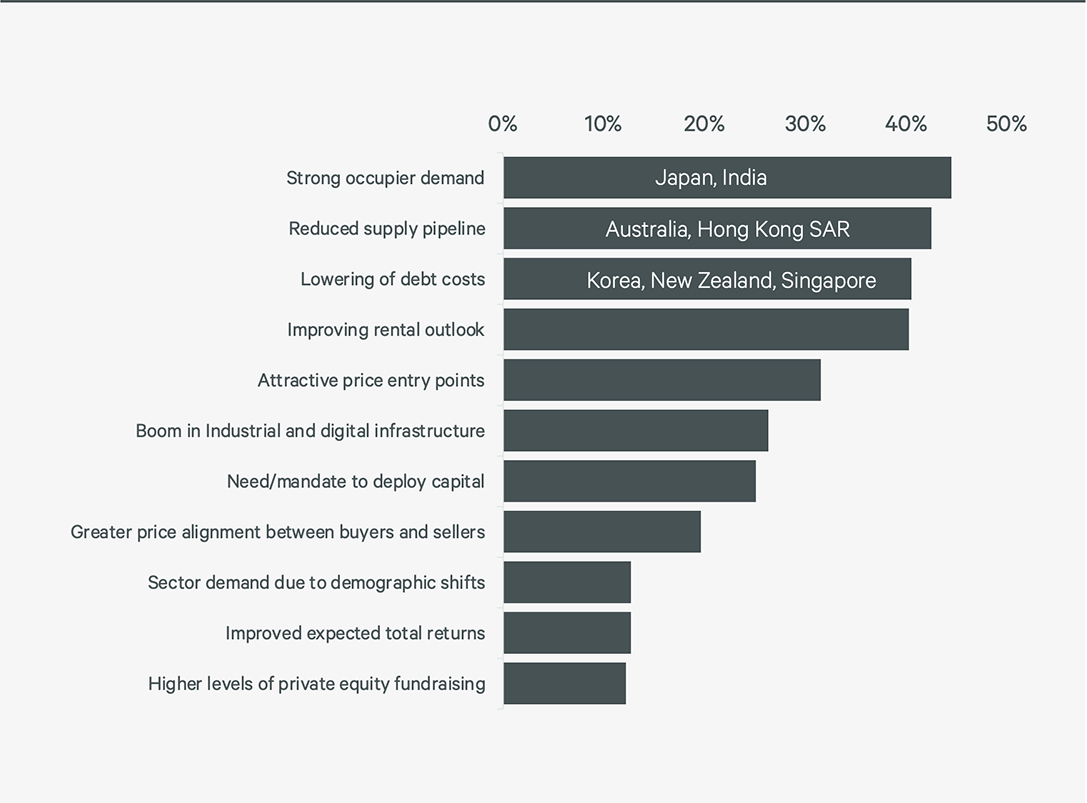

Investors identify leasing demand and reduced supply as major tailwinds

With occupier demand in Asia Pacific remaining strong, investors identified this factor as the biggest tailwind for investment in 2026. This was a particularly popular choice among investors in Japan and India, especially in the office sector, where falling vacancy is supporting a strong rental outlook for 2026.

Due to the ongoing increase in construction costs, the office and retail supply pipeline in many major markets, except for mainland China, has or is about to peak in 2026/2027. Respondents in Australia and Hong Kong SAR investors identified the contraction in supply as their top tailwind for investment in 2026, with the belief that the reduction in the future supply pipeline will help boost investment sentiment in their markets. While new office supply in Hong Kong SAR peaked in 2025, citywide office vacancy remains high, limiting rental growth potential.

While the rate of decline in the overall cost of debt is set to be more limited in 2026 than in 2025, investors in markets including Korea, New Zealand and Singapore still regard the lowering of debt costs as a major tailwind for investment. Singapore in particular has seen a significant reduction in swap rates, with the 3M SORA measuring ~1.2% in December 2025. Overall commercial real estate debt costs are approaching the low 2% range as a result.

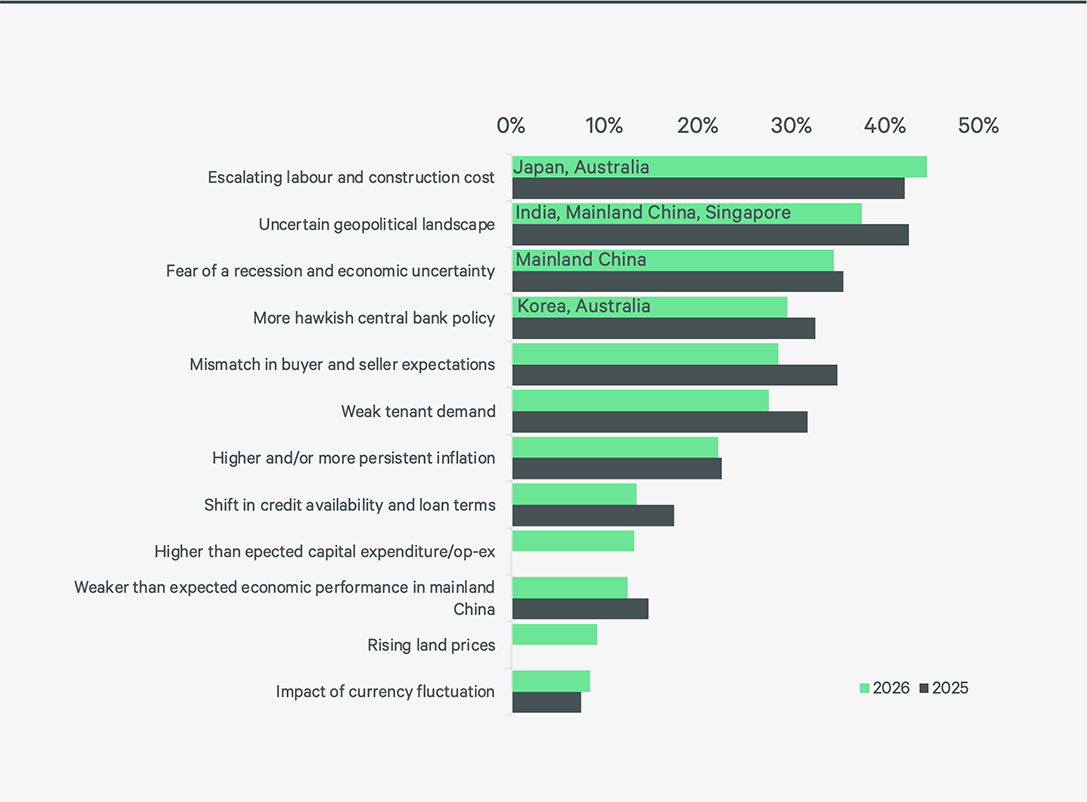

Construction costs overtake geopolitical concerns as main challenge

Escalating construction and labour costs ranked as the top challenge for investors in 2026 for the first time since surveys began. This issue is especially pertinent in Australia, Japan and Singapore, where Turner & Townsend data show overall construction costs for commercial real estate have risen significantly since the beginning of the 2020’s, with economic rents also increasing significantly in these markets.

Investors ranked the uncertain geopolitical landscape as the second top challenge for real estate investment in 2025. While uncertainty around U.S. tariff policy has diminished, investors, particularly those from mainland China and India, continue to display concern about geopolitical tension. These markets generally expect below-trend economic growth as a consequence, with mainland Chinese investors most concerned about the economy.

While still a top concern, investors are less worried about both the mismatch in buyer and seller expectations as well as central policy rates. However, following recent statements from government entities and central policy makers, particularly in Japan and Australia, concerns about potential rate hikes in these markets in 2026 have resurfaced and will be top of mind for investors as further economic data is released.

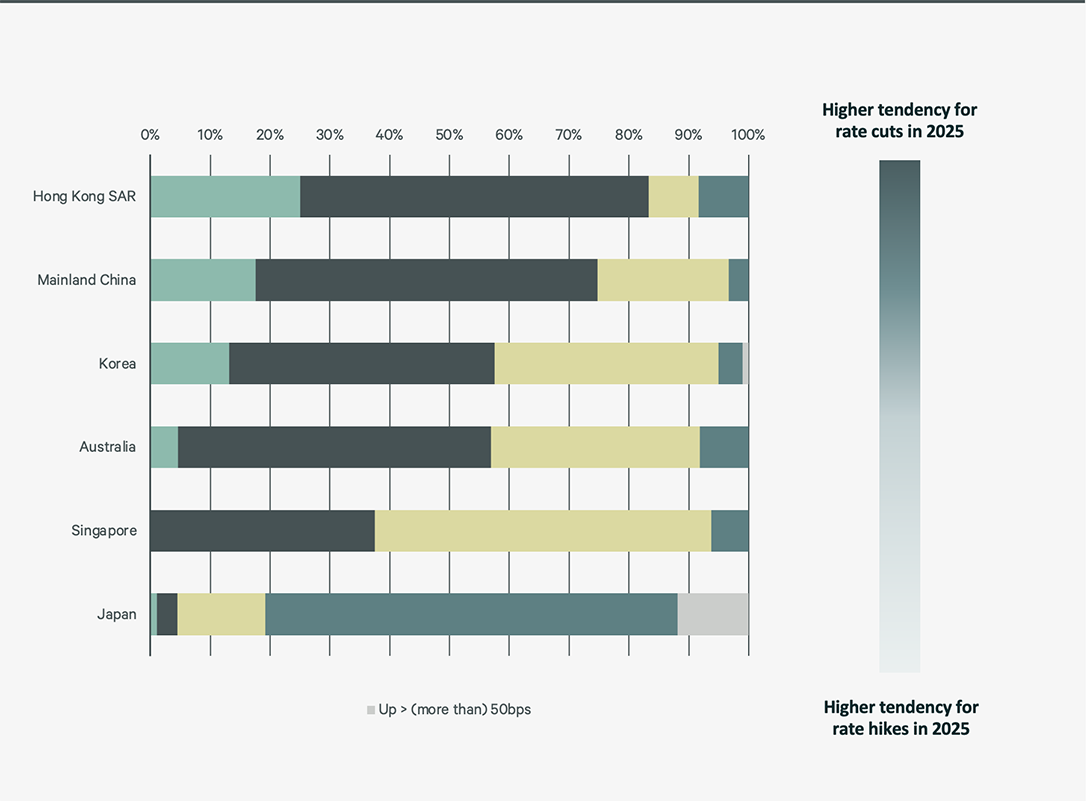

Interest rate cuts expected in some markets; albeit at a lesser magnitude

Most central banks in Asia Pacific implemented significant interest rate cuts in 2025, led by those in Singapore, Korea, Hong Kong SAR and Australia, which announced their first interest rate cuts following the Fed’s move to reduce rates in 2024.

As expected, the Fed lowered the federal funds rate by 25bps in December 2025 to a range of 3.50% to 3.75%, bringing the total magnitude of rate cuts to 175bps during this cycle. The Fed projects one to three further rate cuts in 2026, dependent on both the unemployment rate and inflation. Under the USD peg, investors believe Hong Kong SAR will follow suit in lowering borrowing figures, although the benchmark HIBOR has been volatile.

Investors believe that there will be further rate cuts in mainland China in 2026 as the People’s Bank of China (PBoC) looks to stimulate domestic demand. Although this will result in a further widening of positive cap rate spreads in the country’s commercial real estate market, the supply surplus remains a bigger concern for investors, and in many cases, shorter remaining land tenures are bigger concerns among investors.

Japan raised its policy rate to 0.75% in December 2025 and will conduct further monetary tightening in the coming year as inflation-adjusted real interest rates are negative. As a result, this year’s survey reflects popular expectations of a further rate hike, with a majority expecting any such raise to be within 50bps in 2026.

Key Takeaways:

- Net buying intentions improve across the board, reaching 17% this year, driven by improvements in Korea, Australia and Singapore, and stable buying intentions in Japan.

- REITs, institutional investors and funds to be more active buyers in 2026, while private investors and developers to be net sellers.

- Investors identify strong leasing demand and reduced supply as main tailwinds for real estate investment.

- Escalating construction and labour costs ranked as the top challenge for investors in 2026 for the first time since surveys began. This issue is especially pertinent in Australia, Japan and Singapore.

- Interest rate cuts are expected in some markets, albeit at a lesser magnitude.

Preferred Investment Strategies and Sectors

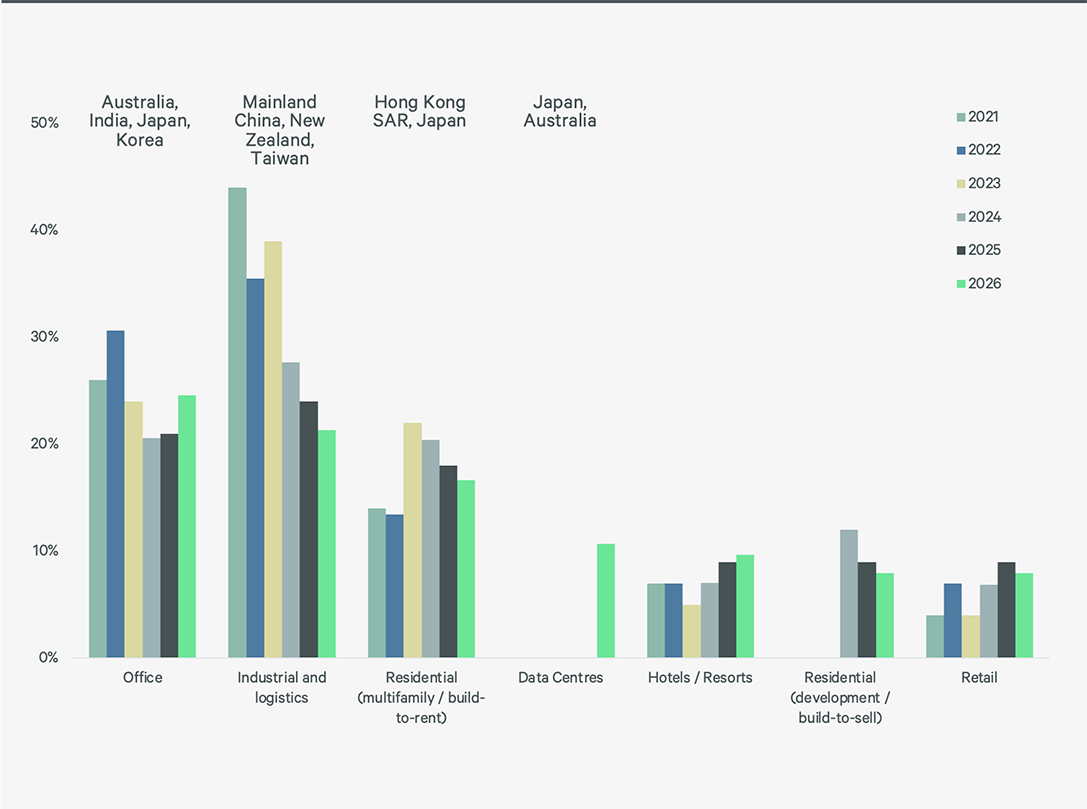

Office overtakes industrial as top sector

Respondents to this year’s survey named offices as the most preferred sector for the first time in six years, with industrial & logistics and the living sector rounding out the top three.

With office leasing activity in many Asia Pacific CBDs picking up, investors are returning to the sector after a period of inactivity. Markets providing strong rental growth such as Australia, Japan, and Korea were the most popular markets for office investment in 2025, with Singapore set to join them in 2026.

2025 saw industrial & logistics rental growth moderate or correct in some markets following the addition of large new supply, leading to a decline in investor appetite for this asset class. However, demand for core, modern logistics facilities remains strong, with mainland Chinese, New Zealand and Taiwanese investors choosing this sector as their top preference. Investing in Korean logistics assets will remain an attractive option as fundamentals in this market continue to rebound.

The living sector remains popular, with build-to-rent and build-to-sell opportunities attracting strong interest. However, a lack of investable properties and policy risks has led to interest in this asset class stabilising after strong growth in demand in recent years.

Hotels and hospitality assets have continued a modest climb in preference for investors for four straight years following strong asset performance since the end of the pandemic. Investors are still keenly interested in strong tourism markets such as Japan and Korea, with opportunities in SEA markets such as Vietnam and Singapore also appealing.

Newly classified as a mainstream sector in this survey, data centres were the fourth most popular asset class for investors in 2026. Investors continue to explore opportunities to build scale in this sector, with both data centre joint ventures and M&A activity increasing substantially over the past 24 months.

Source: 2026 Asia Pacific Investor Intentions Survey, CBRE Research, January 2026.

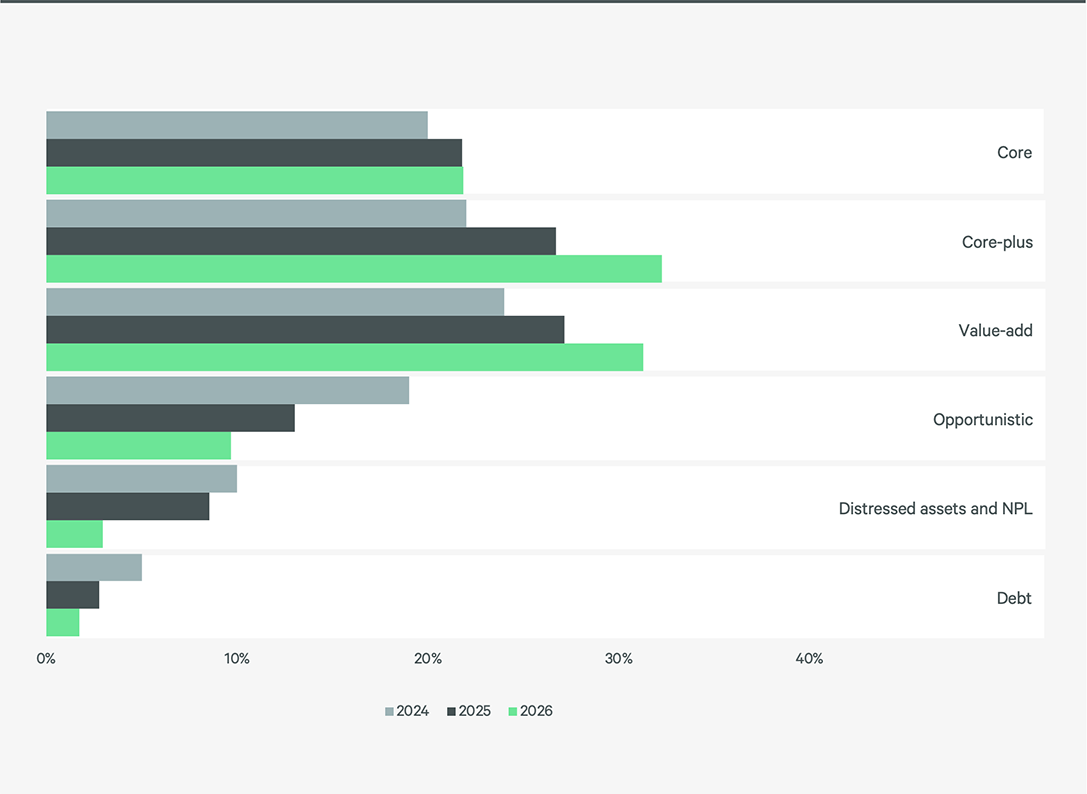

Core-plus and value-add more popular investment strategies; lower interest in opportunistic

Investors’ growing preference for core-plus and value-add investment strategies will remain prominent in 2026, with over 63% of respondents choosing one of these strategies as their preferred option this year. With yield compression across most markets set to be limited in 2026, investors believe they can achieve core-plus and possibly value-add returns from core product as their rental growth conviction grows stronger.

Opportunistic strategies attracted significantly weaker interest from investors in this year’s survey amid declining opportunities for higher IRRs as distressed acquisitions become more limited and appetite for speculative development declines. Development activity also remains limited due to elevated construction and labour costs across the region and lagging economic rents.

Vintage credit strategies such as distressed and debt strategies have fallen out of favour among investors now that traditional sources of debt such as banks are more accommodative. However, credit strategies may still be viable in markets with elevated interest rates such as Australia, although the scale of any such deals compared to previous years will be smaller.

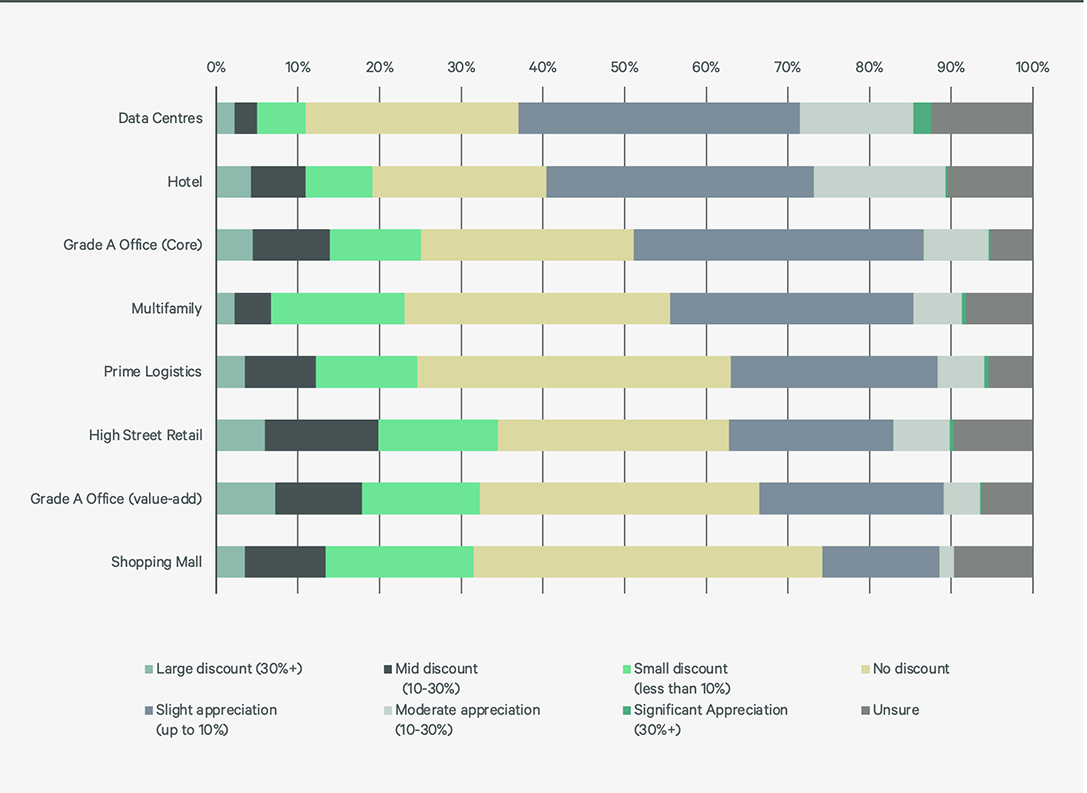

Pricing expectations improve, led by hotels, data centres and core offices

Following a period of adjustment, pricing expectations among investors in Asia Pacific for 2026 have improved, indicating that pricing for prime assets has bottomed out. Only 30% of investors stated their intention to continue to seek discounts for value-add office and shopping mall acquisitions, a significant decline from the 50% who planned to do so last year.

Compared to the 2025 survey, core offices experienced the most significant change in sentiment towards pricing. Almost 50% of respondents now say that they expect some form of price appreciation for core offices in 2026. This comes amid continued investor demand for well located, high quality, and ESG-friendly office properties with high occupancy and strong tenant recruitment and retention capability.

After performing strongly over the past 36 months, investors anticipate further increases in pricing for hotel and multifamily assets over the course of this year. However, CBRE expects this trend to emerge only in a few select locations and among high quality assets.

Investors expect data centres to experience the strongest price appreciation in 2026. While cap rates across most markets for both shell & core and fitted product remain stable, underlying income growth and increased belief in the occupier demand side of the equation will drive any material cap rate compression for stabilised assets.

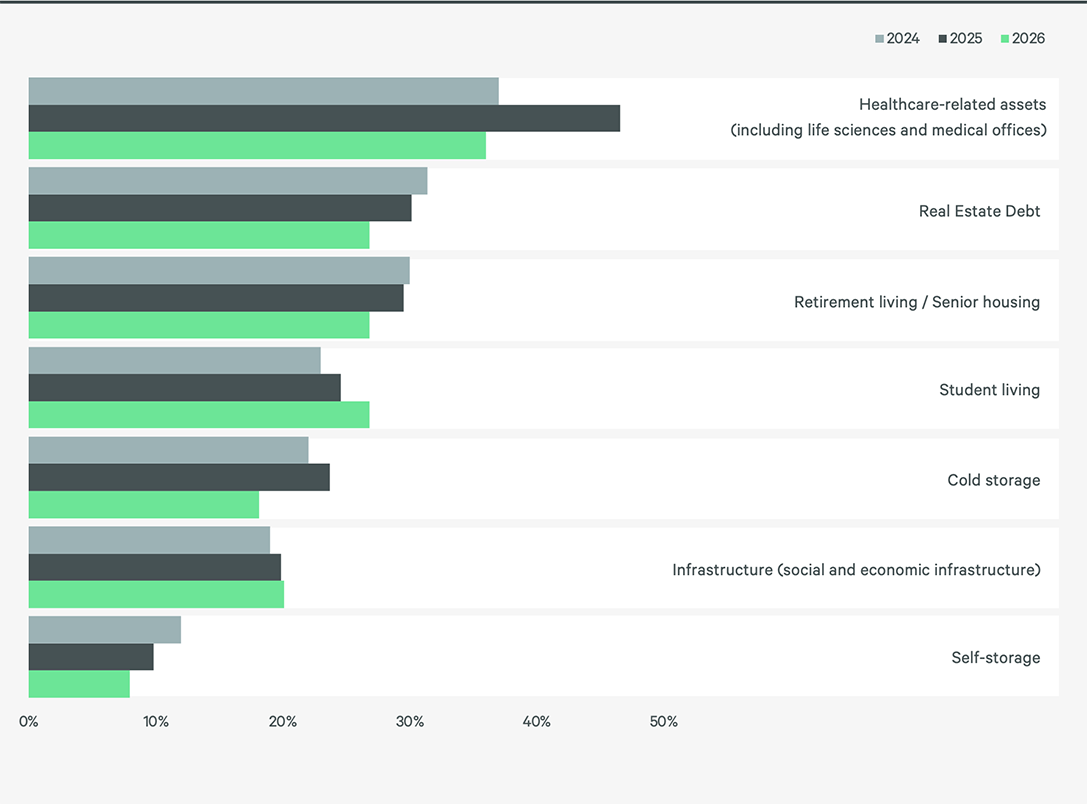

Student living gains traction but interest in alternatives drops slightly from last year

When asked to select the most popular alternative asset for investment in 2026, investors named healthcare related properties, including life sciences and medical offices, in first place for the fourth consecutive year. However, investors cite challenges such as scalability and lack of government funding as obstacles to investment in this sector.

As with more mainstream build-to-rent and build-to-sell assets, investors continue to explore the spectrum of living sector properties. Student accommodation, particularly in markets with high levels of immigration such as Australia and Hong Kong SAR, continues to gain popularity. Retirement living in markets with ageing populations, such as Japan and Korea, also attracted stronger interest in this year’s survey.

Although ranking below other alternative sectors, infrastructure investment interest continues to rise moderately. According to McKinsey, US$106 trillion of infrastructure investment will be needed globally through to 2040 to meet demand for new and updated assets and services.

Source: 2026 Asia Pacific Investor Intentions Survey, CBRE Research, January 2026.

Key Takeaways:

- Office ranked as the most preferred sector for investment for the first time in six years, with industrial & logistics and the living sector rounding out the top three.

- Investors’ growing preference for core-plus and value-add investment strategies will remain prominent in 2026.

- Following a period of adjustment, pricing expectations among investors in Asia Pacific for 2026 have improved, led by hotels, data centres and core offices.

- Student living gains traction but overall interest in alternative assets drops slightly from last year.

Investment Destinations

Tokyo remains top cross-border target; Hong Kong SAR climbs back into top five investment destinations

With cross-border investment activity continuing to see an uptick, Tokyo retained its position as the preferred market for cross-border real estate investment for a seventh consecutive year. Japan's accretive debt costs as well as stable and increasingly growing cash flows continue to lure investors.

Sydney took second place amid sustained demand from investors looking to capture historically attractive pricing and strong fundamental and demographic growth in Australia’s top market. Investors are especially keen on core CBD office product, with several landmark deals settling in 2025 and several more projected to trade in 2026.

Singapore and Seoul tied for third place. Singapore saw a sharp increase in investors indicating a preference for core and core-plus strategies following significant debt cost reductions in 2026. Seoul, which surged from eighth in the previous year’s rankings, continues to establish itself as a top cross-border investment destination following a rebound in dry logistics investment and a diversifying pool of investable sectors (e.g. hotels, multifamily, data centres, etc.).

After a period outside the top 10, Hong Kong SAR ranked fifth in this year’s survey on the back of growing investor interest, particularly from mainland Chinese investors. The living and hotel sectors are top targets, with 2025 witnessing several deals for repurposing underutilised hotel assets into student accommodation for the growing student base; a trend expected to continue this year.

Key Takeaways:

- Tokyo retained its position as the preferred cross-border real estate investment destination for a seventh consecutive year. Sydney took second place, with Singapore and Seoul tied for third place.

- After a period outside the top 10, Hong Kong SAR ranked fifth this year on the back of growing investor interest, particularly from mainland Chinese investors.

ESG and Commercial Real Estate Investment

Investors prefer to retrofit for sustainability rather than buy or develop

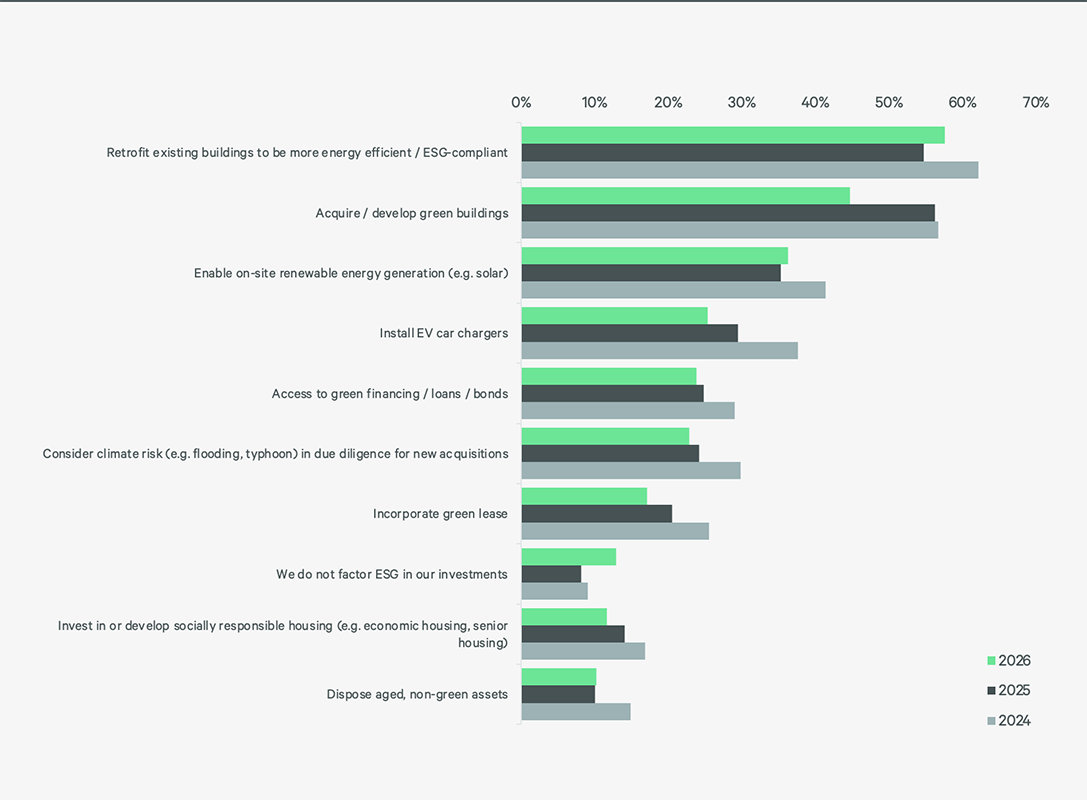

When asked to name the ESG initiatives they plan to pursue when looking at new investments, around 58% of investors, the bulk of which are private equity funds, real estate funds and developers, intend to retrofit existing buildings to be more energy efficient. With elevated construction costs continuing to have a strong bearing on new developments, acquisition/developing green buildings was relegated to second place in this year’s survey. Investors nevertheless remain focused on acquiring green assets.

Investors are still committing to sustainability initiatives that can illustrate the extent of cost savings and attract tenants. This trend is supported by CBRE's 2025 Asia Pacific Office Occupier Survey, which found over 60% of occupiers stating that, for sustainable building features and operations, they would either pay a premium for it or seek a discount/outright reject if it is absent.

Some 36% of respondents indicated that they plan to adopt renewable energy generation, particularly in Asian markets and in the industrial and living sectors. Whilst this is also a popular initiative in the office sector, respondents to CBRE’s 2025 Asia Pacific Office Occupier Survey ranked it as the fourth most important factor influencing their building selection decisions, with tenants prioritising building location, quality and rents in the immediate term.

Source: 2026 Asia Pacific Investor Intentions Survey, CBRE Research, January 2026.

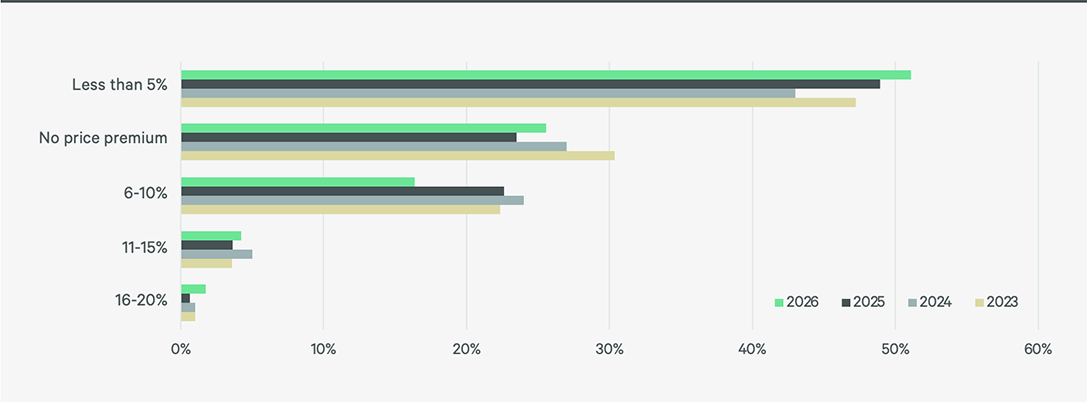

Over 50% of respondents willing to pay 1-5% green premium

With occupier flight-to-quality and flight-to-green demand remaining prominent across Asia Pacific, new premium office buildings are well-positioned to meet the requirements of corporate occupiers seeking to create high-quality workspaces to attract and retain talent.

About 26% of investors displayed little or no willingness to pay a price premium to acquire an ESG certified property, slightly up from 24% in 2025, but down from 27% in 2024 and 30% in 2023. Most of these investors indicated they would pay a slight premium (less than 5%), with 51% of respondents willing to pay slightly more for ESG assets.

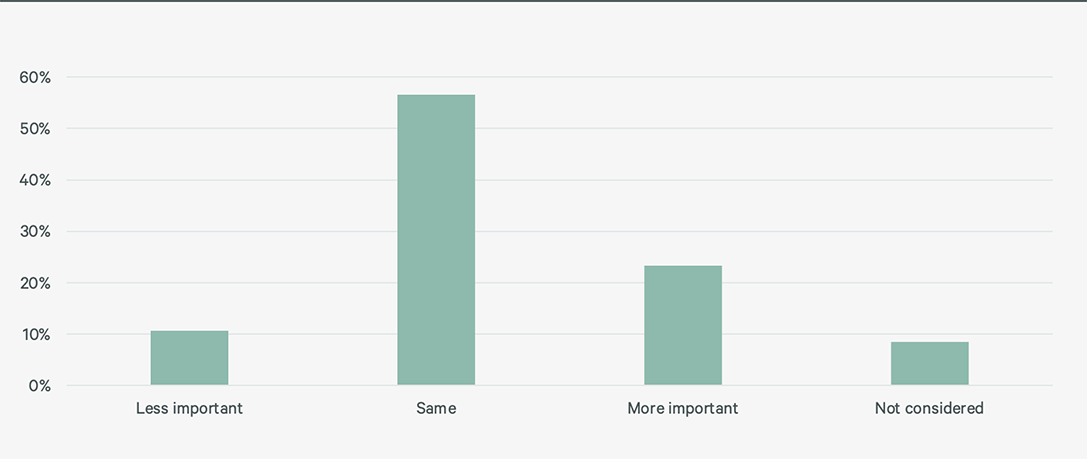

While most investors (57%) indicated that their ESG considerations for 2026 would be the same as 2025, over 23% stated that they would increase their emphasis on ESG when looking at investment decisions in 2026. Australia and Singapore lead the rest of Asia Pacific in green building adoption as authorities in these markets require all new buildings to be green certified. With green buildings set to become the norm across the region along with a global commitment to achieving net zero emissions by 2050, investors are strongly advised to integrate ESG criteria into their investment decisions.

Key Takeaways:

- When looking at investment in ESG initiatives, 58% of investors intent to retrofit existing buildings to be more energy efficient.

- More than half of the surveyed investors are willing to pay a 1-5% price premium to acquire an ESG-certified property.

- Most investors (57%) indicated that their ESG considerations would remain the same as last year, while more than 23% stated that they would increase their emphasis on ESG when looking at investment decisions in 2026.

Research Contacts

Capital Markets Contacts

Greg Hyland

Head of Capital Markets, Asia Pacific

Callum Young

Executive Director, Capital Markets, Asia Pacific

Related Insights

The Asia Pacific commercial real estate market is poised for another solid year in 2026, with both investment and leasing activity forecasted to strengthen, backed by the region's resilient economy.

Nearly three quarters of commercial real estate investors plan to buy more assets in 2026 as prices stabilize and fundamentals improve.

CBRE’s European Investor Intentions Survey 2026 outlines how sentiment and strategy are evolving as the market moves further into its recovery phase.